1 Introduction

1.1 What is Microeconomics?

Microeconomics is often defined as the area of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of limited resources. However, to many economists (including us!) the most interesting aspect of microeconomics is not the subject matter itself but the conceptual framework we use to approach the problem of study. Specifically, we —micro-economists— think of individuals and firms (or, more generally, economic agents) as intelligent seekers of specific goals and postulate that many of the important social phenomena we observe in daily life results from this type of behavior.

A standard use of this framework allows us to study the functioning (and success) of ride-hailing apps such as UBER. A bit more surprising is that we can use a similar approach to evaluate, for instance, the possible impact of alternative policies to reduce crimes in NYC. (You can find here an article about this topic.)

1.2 Conceptual Framework

To explain the observed behavior of consumers and firms —or, more broadly speaking, economic agents— we rely on two simple principles.

Optimization: Agents choose the best (or most desirable) option among all the options that are available to them.

For instance, in the standard consumer problem, we assume that each person buys the most desirable set of goods that he can afford with his income level.

Of course, this optimizing postulate does not fully reflect how people and firms behave in practice. Many cognitive limitations impede agents to behave in such an ideal way. Through the years, alternative behavioral models have being proposed in economics to contemplate these limitations. Nevertheless, the optimizing behavior model is a great benchmark to incorporate these deviations, and it is also still quite used in used in many applications.

Equilibrium: In a market context, prices keep adjusting until demand equals supply.

To illustrate this concept, suppose that one day all tacos on campus are priced at $50. As you can imagine, there will be really few students and professors willing to pay that price! Thus, sellers would end the day with a lot of unsold tacos. To avoid this situation, optimizing sellers will have incentives to lower their price in order to attract more taco customers. This process often iterates till sellers select a price at which the number of tacos made in a specific day roughly equates the number of tacos that consumers are willing to buy. We refer to the latter as an equilibrium price.

1.3 Modeling Approach

Reality can be very complex. Economic models help us to simplify it, so that we can just focus on the key, essential forces or features of the problems we are interested in.

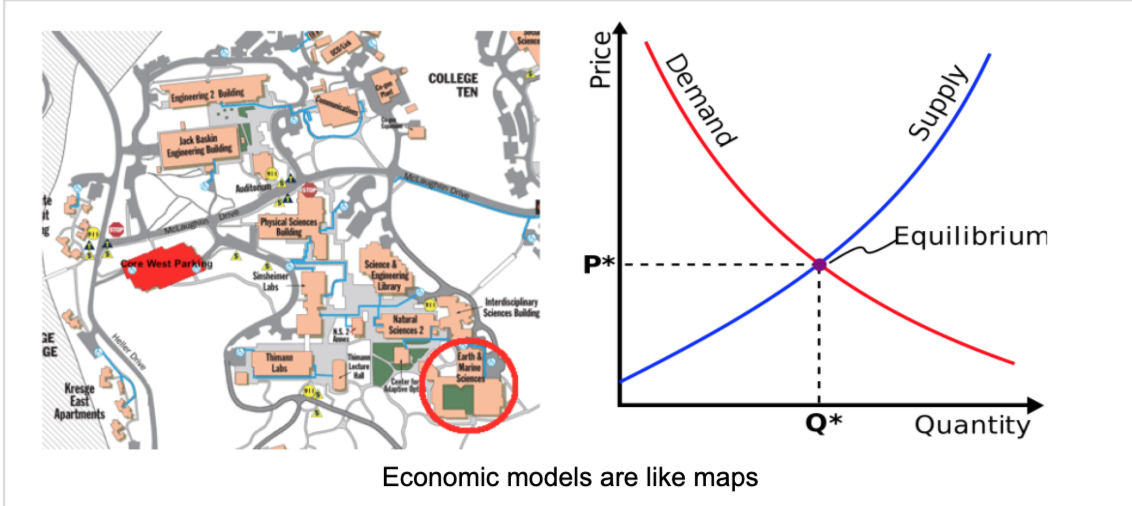

A common analogy to economic models are maps. Though the geography of the world is quite rich, to figure out the best way to go from one specific city to a different one, we can abstract from many of its features and simply focus on basic diagrams. To explain the market price of a specific good, we often behave in the same way. We focus on the key determinants of its demand and supply and assume that other markets remain unchanged.

1.4 Mathematics as a Language

In economics, we often use the mathematical language to express, develop and discuss our ideas. Mathematics helps us to precise our thoughts and avoid logical fallacies in our analysis.